Year-end Adjustment

Overview of Year-end Adjustment

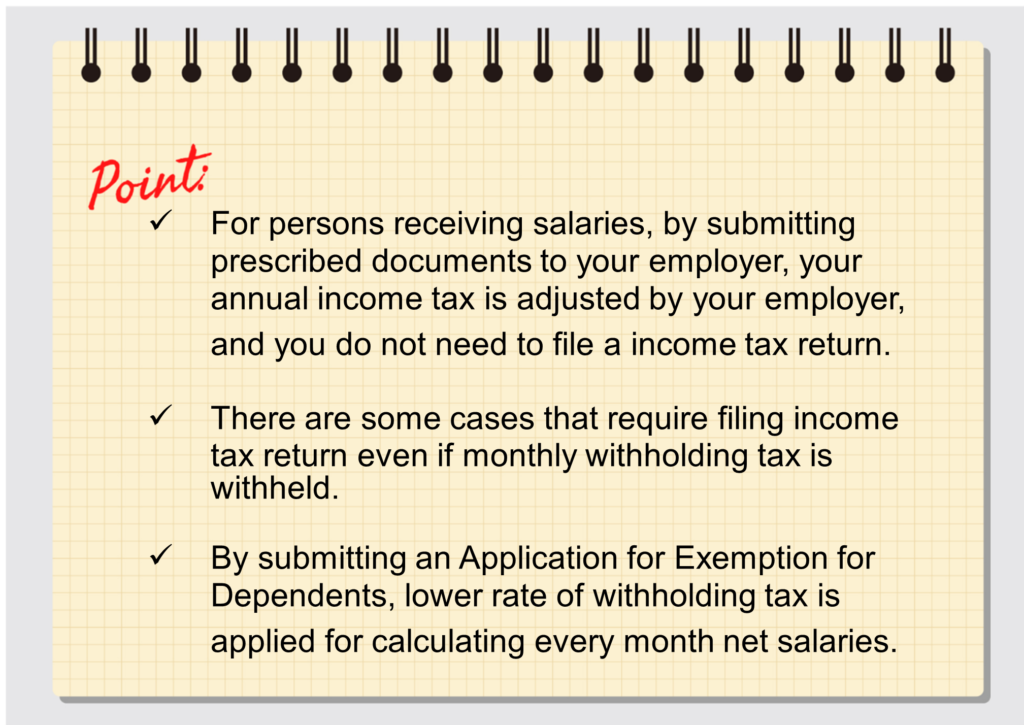

Under the Japanese Individual Income Tax Law, if you are paid salaries, wage, bonuses and other employment income by your employer, income tax is withheld from the income and the employer is required to adjust your annual income tax at the end of year.

Therefore, you are not normally required to file an individual income tax return, except for some cases.

In order for your employer to do your year-end adjustments, you need to submit some documents to your employer.

Documents Required for Year-end Adjustment

In the National Tax Agency home page, there are applications for year-end adjustments written in English, Chinese, Portuguese, Spanish, Vietnamese, Filipino

各種申告書(扶養控除等申告書など)|国税庁 (nta.go.jp)

- Application for (change in) Exemption for Dependents

You need to submit this application to your employer before the first pay day of the year, and you need to submit another application to report any change since the beginning of the year. Thus, usually two sets (for example, at the end of 2022, one for 2023 and one for any changes in 2022) are submitted.

By submitting this application, lower rate of withholding tax is applied in calculating monthly net salaries.

- Application for Basic Exemption and Exemption for Spouse

In order to apply for a basic deduction, maximum of 480,000 yen, this application must be submitted. Also, by filling out information about your spouse’s estimated salaries and etc., you may be qualified for a spouse deduction.

- Application for Deduction for Insurance Premium

If you paid life insurance premium, earthquake insurance premium, and social insurance premium other that those withheld from your monthly salaries, you should submit this application for deductions for insurance premiums, together with proof of payments issued by insurance companies.

Cases that Require Filing a Tax Return

Exempted from year-end adjustment means basically you need to file a final income tax return.

Common cases that require filing income tax return are:

- Your total salaries, wage and bonuses exceeds 20,000,000 yen for a year

- Beside your salaries from one employer, you have other income of more than 200,000 yen

- If you receive salaries and wages from two or more sources and they are all subject to withholding tax, the sum of non-primary salaries and total other income exceeds 200,000 yen